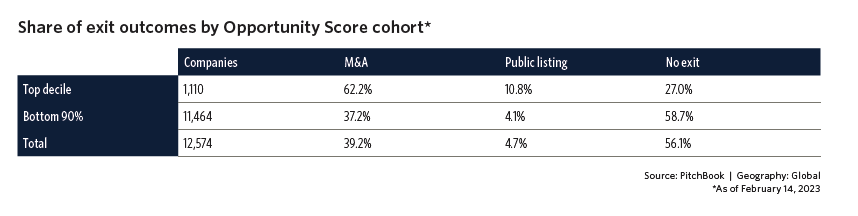

It is every startup’s dream to go public. An IPO is the pot of gold at the end of the startup rainbow. As one of my startup friends says “All the blood, sweat, and tears will be worth it. I will finally get my dream Malibu beach house!” The unfortunate reality is that according to recent research by PitchBook of a cohort of 12,574 VC-backed firms from 2018, only 4.7% achieved an IPO. 39.2% achieved an exit via M&A, and the remaining 56.1% had no exit. SaaS companies raising VC investments are loath to talk about a non-IPO exit. Perhaps it is time for management teams to seriously consider having a ‘Plan B’ if their trajectory to an IPO looks shaky.

In this article, we will discuss:

- The PitchBook Data

- Maybe It Is Time for Your SaaS Startup to Have a Plan B

- How to Build an Under-the-Radar M&A Exit Strategy 3

- Understand M&A Options

- Be Realistic About Exit Valuations

- SEG SaaS Index: Public Market Multiples

- Private SaaS Companies Are Valued Less Than Public SaaS Companies

- Identify Potential Acquirers

- Qualify Potential Acquirers

- Network with Potential Acquirers

The PitchBook Data

PitchBook is a phenomenal source of quantitative data about VC and private equity-backed companies. PitchBook is a financial data and technology company that provides comprehensive data on private equity, venture capital, mergers and acquisitions, and other alternative assets. PitchBook recently released the PitchBook VC Exit Predictor, an AI tool that leverages machine learning and its vast database of information on VC-backed companies, financing rounds, and investors— to provide objective insights into startups’ prospects of a successful exit.

Pitchbook estimates that there are 120,000 active VC-backed companies.

The goal of the VC Exit Predictor is to use AI to predict the exit outcome of specific companies (IPO, M&A, No Exit). PitchBook backtested a cohort of 12,574 companies active since 2018 to build a model they could use for future predictions. The data used to train the model has some startling insights:

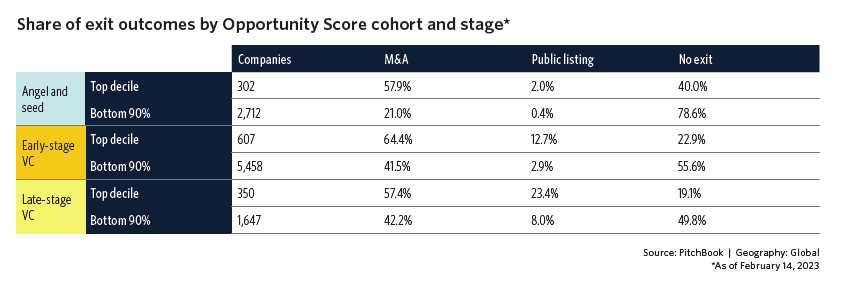

Top decile firms had superior revenue, revenue growth rates, profitability, and valuations in comparison to their peers. Top decile firms had an order of magnitude better outcomes than the bottom 90%.

Maybe It Is Time for Your SaaS Startup to Have a Plan B

More than half of the companies in PitchBook’s analysis achieved no exit – either they failed or became self-sustaining with no additional VC investment. If your SaaS business has become self-sustaining it is a win for you, your employees, and your customers. If you are looking for a substantial payday, then M&A is the next best choice.

Investors look down on potential investments that explicitly state their exit strategy is M&A. As a result, many management teams do not build an effective M&A strategy until it is too late. Trying to sell your company when revenues are declining or cash has run low is very, very hard.

Instead, you should build and execute an M&A exit strategy as a normal, low-key part of your business. It always pays to have options.

How to Build an Under-the-Radar M&A Exit Strategy

There is a four-step process if you decide to explore M&A as a potential exit strategy. You can do this on your own without hiring an investment banker or a broker. Your board of directors should be cognizant of what you are doing. The major steps in an M&A exit strategy include:

- Understand M&A Options

- Be Realistic About Exit Valuations

- Identify/Qualify Potential Acquirers

- Network with Potential Acquirers

Understand M&A Options

Before you begin you need to understand that M&A can be driven from many perspectives. You need to figure out how your company could possibly fit into an acquirer’s strategy. There are three basic types of Mergers & Acquisitions – Acceleration Deals, Diversification Deals, and Consolidation Deals.

Acceleration Deals

Acceleration deals are opportunities that significantly accelerate a firm’s ability to enter and grow in a market. They are the Buy portion of the typical Buy-Build-Partner decisions companies make every day. Microsoft’s investment in OpenAI is a classic example.

Acceleration deals also tend to be the most lucrative. A quintessential example is Google’s 2006 $1.65 billion acquisition of YouTube. YouTube had been founded a year and a half before and had raised $85 million in venture capital. They had 65 employees but controlled 46% of the video streaming market. Google had been struggling in that market with Google Video. The YouTube acquisition was a huge bet, but it enabled Google to dominate the video streaming market. In 2022 YouTube had grown into a $29 billion business.

Diversification Deals

Diversification deals focus on expanding into new or complementary markets. Let us assume that your firm is currently in the warehouse management market, which is part of the overall supply chain management market. In supply chain management there are five major sub markets – supply chain planning, supply chain manufacturing, supply chain distribution, supply chain sales, and supply chain services. Warehouse management is part of the supply chain distribution segment. Other sub-segments include inbound logistics, outbound logistics, transportation management, vendor managed inventory, global trade management, etc.

When considering diversification opportunities you want to look for sub-markets/solutions/companies that complement your existing solutions. Your current customers should use a targeted company’s solutions. The buyers of the solution (economic, using, and technical buyers) should be similar to the buyers for your solutions. Your existing solution should provide either inputs to the targeted solution or process outputs from your solution. Diversification opportunities provide a way to accelerate your revenue and profit growth at a significantly lower risk than developing, marketing, and selling your own solution.

Consolidation Deals

Consolidation deals focus on acquiring and integrating companies that offer similar solutions to your current solutions. Basically, you use your current business as a platform and consolidate non-critical business functions like marketing, customer service, professional services, finance, HR, accounting, facilities, data centers, and hosting operations of acquired companies into your platform. Research & Development as well as sales tend to remain as standalone units.

In the 1980s and 1990s companies like Computer Associates, Platinum Technology, and Sterling Software were classic consolidators. I was the Group VP Business Development for Sterling’s Application Management Group in the late 1990s where I was responsible for a number of acquisitions and divestitures. In today’s market companies like Oracle, Gores Group, and OpenText are active and successful consolidators.

Consolidation typically occurs in the latter stages of the Technology Adoption Lifecycle – usually Late Majority or Laggards. It is predicated on the assumption that a company’s expenses can be significantly reduced through the consolidation of non-critical overhead functions. Also, economies of scale can be realized through the integration of marketing, sales, operations, and professional services and the cross selling of products and services into the assembled customer base. The acquiring company obtains the benefit of increased revenues and profitability.

Be Realistic About Exit Valuations

How much is your privately-held SaaS company worth? Many management teams have exceptionally high opinions of what their company is worth. This can stop an exit strategy before it starts.

The best way to honestly determine the valuation of a privately held SaaS company is to obtain a 409a valuation. The 409A valuation process typically involves engaging an independent valuation firm to determine the fair market value of the company’s common stock, taking into account a variety of factors such as financial performance, market trends, and comparable transactions. The valuation report produced by the firm serves as evidence to the IRS that the company’s equity-based compensation was issued at fair market value, which can help to avoid potential tax penalties. Most 409a valuations discount private SaaS companies b 20% to 30% of their public peers.

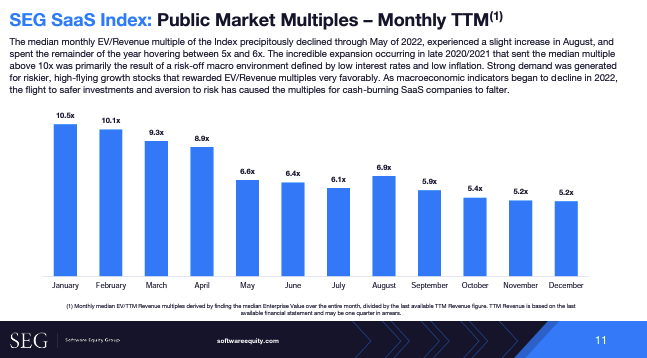

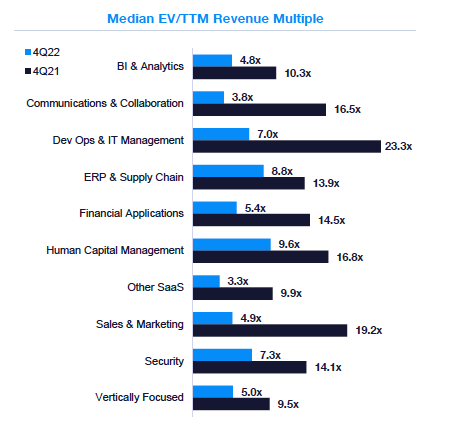

There are some free public sources of SaaS valuations. The Software Equity Group (SEG) regularly publishes quantitative research on the software and SaaS market M&A activity. The SEG SaaS Index contains dozens of publicly traded SaaS companies. They recently published their SEG 2023 Annual SaaS Report. It provides a ton of data on SaaS valuations and financial operating metrics. The impact of the market downturn can be clearly seen across all categories of SaaS.

Some excerpts include:

SEG SaaS Index: Public Market Multiples

Valuations vary by industry segment:

Private SaaS Companies Are Valued Less Than Public SaaS Companies

There are a lot of reasons why private companies are valued less than public companies. In general, there are three major factors and six minor factors:

Major Private SaaS Company Discount Factors

- Liquid equity

- Audited Financials

- SOX 404 certifications

Minor Private Company Discount Factors

- Revenue Scale & Growth Rate

- Market Size

- Revenue Retention Rate

- Gross Margin & Revenue Mix

- Customer Acquisition Efficiency

- Profitability

You need to understand all the factors that impact your valuation – you can’t apply public company valuation metrics to privately-held SaaS companies. For more information check out Public-Private SaaS Valuation Gap Now Over 50%

Identify Potential Acquirers

The next step is to build a list of potential acquirers and qualify each company. Using your understanding of potential deal scenarios (Accelerate, Diversify, Consolidate) build a list of potential acquirers. Leverage your company’s existing competitive analyses to identify obvious candidates. Build a map of Competitor Revenue/Headcount/VC Funding. Check out this article for more details on how you can do this using free resources.

Qualify Potential Acquirers

The next step is to investigate the candidates you have identified and determine if an acquisition is even feasible. Some topics you should explore include:

- Do they have a history of doing acquisitions? What types of deals have they done (Accelerate, Diversify, Consolidate)? What types of valuations have they paid? How have they handled the integration?

- What is the potential strategic fit?

- Do they have the currency (cash, stock, debt) to fund an acquisition?

- Who could be the key players/influencers that could make a deal happen?

You need to focus on candidates where your business can offer real value to the acquirer. Everybody would like to get acquired by Google at a YouTube-like valuation. Unfortunately, few are a great fit.

Network with Potential Acquirers

The last step is to begin an ongoing networking process with potential acquirers. Most deals evolve over a long period of time. Your CEO, VP Marketing, VP Sales, CTO, and CPO should take the opportunity to meet informally with their counterparts. The goal of these discussions is to learn about each other and find ways to collaborate in a non-competitive manner.

As a senior corporate development executive for several public and private equity-backed SaaS companies, I spent about a quarter of my time in informal ‘get-to-know-you’ meetings. When my CEO traveled out of town I made a point to see if I could set up some informal meetings. With the pandemic and the normalization of Zoom meetings, the opportunity for quick meetings is virtually limitless.

It is important that this be an ongoing process. If you wait until you are in a position where you have to sell to survive then you are doomed to fail.

Also published on Medium.