This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

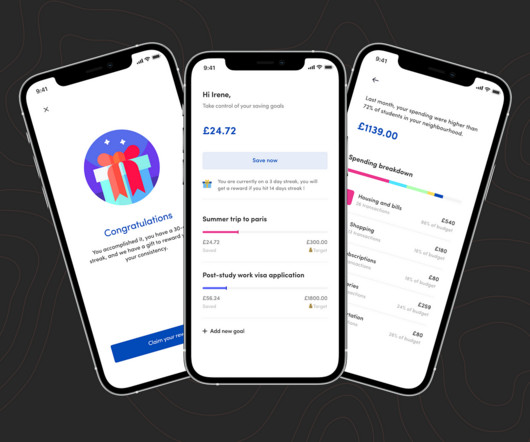

Written by Alex Kreger and UXDA team Digital banking has undergone significant transformation over the past decade, yet many users still experience stress and confusion when managing their finances online. In digital banking, small positive experienceslike celebrating a $5 savingscan have a surprisingly big impact.

This is the effect of Dopamine Banking, where finance meets emotions and entertainment, and every tap of your smartphone is engineered to delight and reward. Traditional banking often struggles to capture and maintain customer engagement. Traditional banking often struggles to capture and maintain customer engagement.

Chasing the next big product win in banking or fintech? For decades, banks competed through branch locations, branding and fee structures. Any banking app that feels generic, uninspired or offers little real value is already lagging behind. billion people worldwide were expected to use mobile banking appsup from 2.7

Why a Brand Matters More Than Ever in the DigitalAge The accelerating shift to digital banking and Fintech solutions means customers interact with financial service providers through multiple digital channels-mobile apps, websites, smart watches, social networks, third-party services, voice assistants and more.

Not to worry; this article isnt about your habits but about helping you build positive habits like saving. By providing modest incentives or bonuses for creating savings accounts or keeping deposits, banks and financial platforms can promote saving. We all have habits, some good and some bad. Human wants are insatiable.

A deep dive into how artificial intelligence is shaping the next generation of financial user experiences — through metrics, strategy, and real success stories Until recently, most banks and financial organizations treated artificial intelligence (AI) as tomorrow’s experiment. IDC estimates the banking industry will invest about $31.3

Listen now: YouTube // Apple // Spotify Brought to you by: Brex —The banking solution for startups Paragon —Ship every SaaS integration your customers want Coda —The all-in-one collaborative workspace Jake Knapp and John Zeratsky are the co-creators of the Design Sprint (the famous five-day product innovation process) and authors (..)

Take the commercial lending function in a bank for instance, and look at a few of the common jobs people perform in each of the four functional areas below. The jobs dashboard is your way of serving the meal in easily digestible portions. The best way to illustrate the value of the jobs dashboard is with an example.

Expect a high-level discussion of your background relevant to the role and what you’re looking for in your next position. Create a story bank of anecdotes that highlight these skills to prepare for behavioral interview questions in particular. Discord Interview Tips Discord values collaboration and belonging.

Supply is thus positively correlated with the price index. These assumptions appear to be confirmed by recent moves from central banks. It is based on two core principles: All else equal , companies seek to maximize margins and will try to increase sales as the price index rises.

Banking apps celebrating feature adoption miss the point of their mobile applications. This gap between user behavior and intention creates massive blind spots, which can be fixed with user feedback and qualitative data: Users complete onboarding (positive metric) while feeling confused and planning deletion (negative intention).

The most powerful thing has been enabling marketers to be able to set up flows without dev assistance because we’ve got this growing bank of data that allows us to segment and change different rules. – Overall, real users feel positive about Appcues. What users say about Appcues Do users feel like Appcues is worth it ?

User research requires you to adopt a position of uncertaintyyoure essentially saying I dont know what we need todo. This can be uncomfortable for some people, as you need to embrace a position of vulnerability where youre not confident what the solutionis. But user research is different.

Gainsight recently announced that we were named a Leader in the first-ever Gartner Magic Quadrant for Customer Success Management Platforms ; Gainsight was positioned highest on the Ability to Execute axis and furthest on the Completeness of Vision axis.

Listen now: YouTube // Apple // Spotify Brought to you by: Brex —The banking solution for startups Productboard —Make products that matter Coda —The all-in-one collaborative workspace Varun Mohan is the co-founder and CEO of Windsurf (formerly Codeium), an AI-powered development environment (IDE) that has been used by over 1 million (..)

JPMorgan Chase is the unified company of its two brands: Chase, a consumer and commercial banking brand, and J.P.Morgan, an investment brand for corporations and governments. System Design Design a real-time fraud detection system for a banking application. Design a real-time notification system for banking alerts.

Today, brute force doesn’t cut it, nor does positional authority; it’s the art of influence… and this can be highly nuanced because you’re trying to shape perceptions of others. You may also be in a better position to ask for and receive assistance in a project or other endeavor. This is also part of the elusive influence puzzle.

And ultimately, the project manager needs to ensure they know how the project fits within the strategic intent that they’re position. And you’re and you and people see this positive behavior. I’ve worked at the bank up in I think it was up in Canada. All of these are vital. You’re earning trust.

One bank (like many of our customers), for instance, was struggling with siloed IT functions. When the IT team is bombarded with constant alerts—many of which are irrelevant or false positives—it becomes increasingly difficult to distinguish between critical incidents and routine anomalies.

Alkami transcends the traditional role of a digital banking software and creates first-class user experiences that fuel long-term growth. Despite facing uncertainty, this Challenger prioritizes creating positive impacts for those they serve, looking beyond mere products and strategic plans. The Architect Award Goes to Alkami!

I learned a lot about product positioning long before I ever stepped into a product marketing role. I think of demos as verbal product positioning. The Product Positioning School of Hard Knocks Early in my pre-sales demo career, I had some demos where my audience was totally engaged and it felt like I hit it out of the park.

Prior to iFundWomen, Maya held positions at JPMorgan Chase and Techstars. Previously he worked for two of the UK’s largest banks, RBS/NatWest and Barclays, on their Mobile Banking apps, and most recently for The Sun, one of the world’s largest online publishing brands, where he was responsible for their news apps.

Between heavy increases in usage as well as staggering drops in economic activity, 2020 was a roller coaster for banks, insurance companies, budgeting apps, and everything in between. On the flip side, they directed anyone who answered “Yes” to the Love Dialog to leave a positive review on the app store. stars to four stars.

While we saw DAU (daily active users) stay pretty consistent for traditional banking apps since the pandemic hit, it spiked for budgeting apps and other mobile-first brands. Historically, the banking experience has never been one to write home about. Let’s unpack that a bit more. And right now, human connection is everything.

Another challenge comes with the unique loyalty customers feel towards their financial institutions and banks. Inefficient customer service is one of the main reasons why customers leave their banks or financial tools. Bank offers Face ID and Wells Fargo has 128-bit encryption to mask sensitive information.

Innovation-thinking banks and fintech startups use natural language processing to augment intelligent chatbots into the customer experience. Banks can use NLP-powered chatbots to provide 24/7 customer assistance and personalized insights based on real-time financial data analysis.

Customers are then able to access the Apptentive product suite to send ratings prompts, survey customers for product information, use Message Center for customer service, send notes to drive positive outcomes, and push customers to upgrade to the latest version of their app.

Melissa begins by describing how there are over 11,000 open Head of Product positions available in the EU today – one of which could be yours. How can you position yourself well now for a future as a product leader, and, once you get the job, what do you do? Plan Your Future Today.

Thousands of employers across all areas of product, from management to design, from digital to physical, are looking to fill positions from our community. . Associate Product Manager @ Bank of America (New York). Each week we highlight some of the recently posted openings. Check out this week’s newest, below….

A UX researcher at the largest Hungarian bank. Such a positive outlook didn’t happen overnight. To end on a positive note, the world of research has expanded incrementally. The post The positive effects of the pandemic on UXR appeared first on UX Studio. Luckily, I was wrong.

Consumers used Finance apps for the same standard purposes, although DAU spiked as people used mobile as their primary access point to banks and finance management. Banking (banks and credit unions), and Insurance (auto, home, life, renters, pets, etc.). Finance brands were generally spared by the marketplace shakeup of 2020.

However, I quickly discovered that there’s too much brand risk for a trusted bank to take this type of lean startup approach. Venus quickly became the key to getting everything done, including getting us a new banking licence! People were extremely privacy-conscious in Hong Kong and banks were trusted.

One of the most important tasks we’re faced with in business and in our personal lives is taking care of our finances, and mobile banking is already insanely popular across all demographics. According to Apptentive’s recent consumer survey , the majority of banks and credit unions offer mobile banking apps—and they are wildly popular.

Itamar highlights three types of product launches: Positive – where a product is launched and is incrementally improved upon. At Google and Bing, only 10-20% of experiments generate positive results. Then these results can then feed back into our ideas bank and update our ICE scores. These are very rare. Linus Pauling.

VR Banking? Take banking for example. Banks have faced serious pressure over the last couple years to make the move to mobile, since that’s where their customers live. On-the-go is when customers truly need access to their bank accounts, so mobile apps and cheque scanners make sense. It’s not Just a Matter of Resources.

This should resonate with anyone in a product role because it refocuses a “No” into a positive but realistic approach. Photo by Clay Banks on Unsplash Now you aren’t building up roadblocks to success, you’re throwing out challenges to be met as a team. If” is positive, but realistic. Yes, if’ is the approach of a deal maker.

Now imagine the same scenario but this time, rather than a machine, you’re inside the bank speaking to a human cashier. In the Kano model, the surprise touches that users enjoy are called “delighters” For example, imagine a staff member handing a free lollipop to your child to keep them happy while you queue at the bank.

By the time you see revenue (or a lack of it)—whether it’s in a dashboard, cash in the bank, or a cancellation notice from a churned customer—it’s too late to take corrective action. As the product changes, the customer behavior changes should positively contribute to a company’s desired business outcome. Tweet This.

The first sign that the thieves were on the move came when Tristan, CEO of a startup accelerator, was contacted by his bank, Monzo , through their app. Unfortunately, Tristan still had to handle charges on cards from two other banks. Using customer support to drive loyalty, engagement and revenue. 1 obstacle for these executives.

Having spoken at conferences twice this year on the subject of design and emotion, I was spurred into writing this post by the number of people who gave me positive feedback. We tend to remember the peak of the experience (whether positive or negative) rather than the end-to-end experience. Why is Designing for Emotion so Important?

I call this type of trust-building process in relationships a “trust bank account.” Relationships are like bank accounts because you make deposits and withdrawals. If you are relatively new in your position and now find yourself working remotely, you have to go first and make deposits. Do what you say you will do.

Banking, fintech, and insurance companies are uniquely positioned to build relationships with mobile consumers—but few tap into their app’s full potential, leaving missed connection opportunities on the table. If you’re in finance, it’s time to reevaluate how you use your app for feedback collection and relationship building.

This is what you want to design for – you can ship a first version with machine learning that’s not amazing, but it doesn’t really damage the end user experience, because the design makes the cost of false positives relatively low. What was the cost of a false positive going to be? Would end users be glad to see the bot?

Stay positive. 27:01] Open innovation at DBS Bank: Over the past few years, DBS Bank transformed into a digital pioneer. Stay positive. Empowered—you can’t innovate until you go and do something. [5:35] 5:35] What are some hacks for being better innovators? [5:47] Reframe worries as opportunities. [8:37]

We organize all of the trending information in your field so you don't have to. Join 96,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content